I'm preparing for a mid-August presentation on CMS data in D.C. - the annual Next Gen Dx meeting.

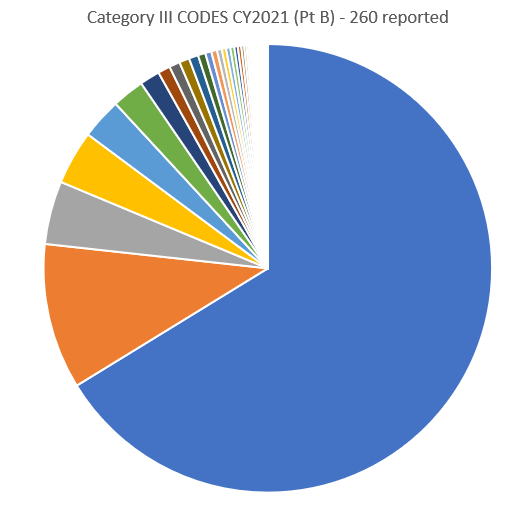

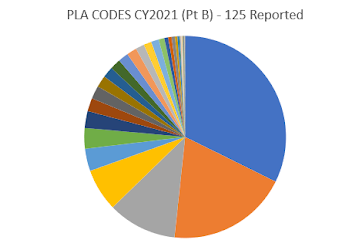

One topic will be the proliferation of Category III and PLA codes, with hundreds active at any given time. But it's a winner take all environment, with a 2 or 3 codes having over half the payments, and no more than 10 having nearly all the payments. This is based on CMS Part B data for CY2021.

- Unexpectedly, a tie-in to a JAMA Health Forum article this week by Sexton, Makower, and colleagues, on delays to LCDs and NCDs for new devices - here.

- See abstract & AI summary of Sexton here.

PLA CODE CONCENTRATION

For 130 PLA codes (and a few "M" administrative MAAA codes). Spending was $230M, with $75M and $45M for the top two codes (50%).

2/3 of all Cat IIi spending, 66%, or $122M, went to the biggest code, an ophthalmology code with 103,000 services, 0191T.

The top ten Cat III codes had about 95% of all Category III spending. That means Codes #2 to #10 had about 30% of spending, leaving 5% for all the remaining 250 codes.